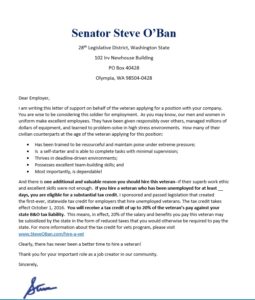

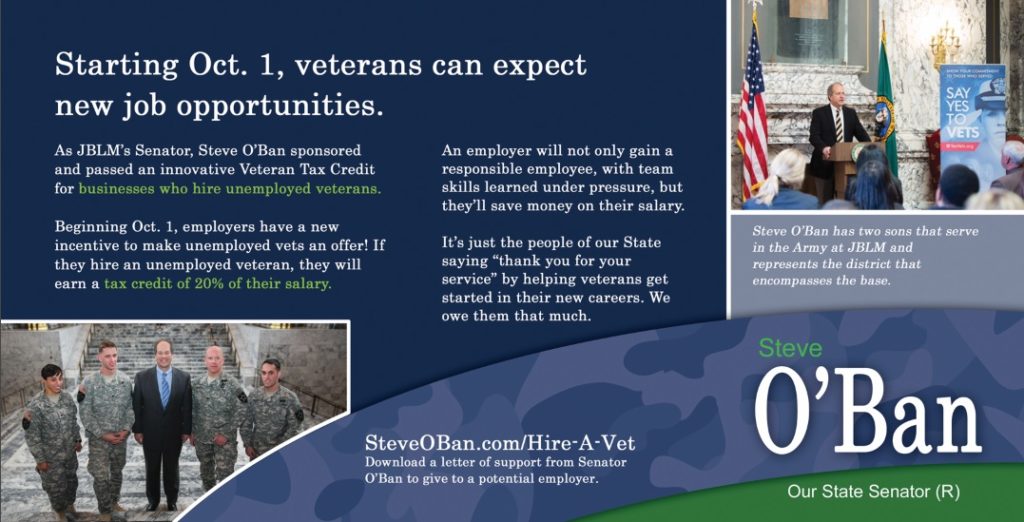

Tax Credit for Businesses that hire Veterans

Download this letter from Senator O’Ban to your prospective employer.

If you are a veteran who has been unemployed for at least 30 days, help is on the way. Beginning Oct. 1, 2016, a new program begins, which was sponsored by Senator Steve O’Ban.

Veterans, download a letter to prospective employers here, and take it with you to your interview, or submit it with your application!

Below is reprinted from the Dept. of Revenue. You can download this information here.

Below is reprinted from the Dept. of Revenue. You can download this information here.

If you as a veteran or a business owner have any questions about this process, contact the DOR. If you have further questions, feel free to reach out to Sen. O’Ban personally at steve@steveoban.com.

Businesses hiring unemployed veterans for full-time employment positions located in Washington beginning October 1, 2016, are eligible for a credit against their business and occupation (B&O) tax or public utility tax (PUT). (RCW 82.04.4498 and 82.16.0499) You can earn credits through June 30, 2022. You must claim all credits earned by June 30, 2023.

How much is the credit?

The credit equals 20 percent of the wages and benefits you paid to or on behalf of a qualified employee, up to a maximum of $1,500 for each qualified employee hired on or after October 1, 2016.

There is no limit on the total credit an employer may receive. However, the total statewide credits may not exceed $500,000 per fiscal year.

The amount of credit you claim during a reporting period cannot be more than the amount of your B&O tax and PUT owed during that period. The same credit may not be claimed for both B&O tax and PUT.

How do I earn a credit?

You earn a credit by employing a qualified employee for a position located in Washington for at least two consecutive full calendar quarters on or after October 1, 2016 and before June 30, 2022.

How do I calculate the credit?

You calculate the credit on 20 percent of the wages and benefits you paid to the qualified employee, or on behalf of the qualified employee from the time the employee was hired through at least the first two consecutive full calendar quarters of employment. You may earn additional credit for wages and benefits paid during future reporting periods until you reach the individual cap. The cap is $1,500 per qualified employee or $500,000 for the statewide fiscal year cap.

Example: Employee is hired on October 1, 2016. The credit equals 20 percent of the wages and benefits paid by you to the qualified employee or on behalf of the qualified employee through March 31, 2017. Credit may be claimed on the March 2017 or Quarter 1, 2017 return. Wages and benefits paid during the next reporting period may be claimed on future returns until the credit of $1,500 per qualified employee or the $500,000 statewide fiscal cap is met. For further instructions, see example under the How do I claim the credit section.

How do I claim a credit?

- Credits are available on a first-in-time basis.

- You may claim a credit, if the qualified employee has been employed by you for at least two consecutive full calendar quarters.

Example: You hire a qualified employee on October 1, 2016 (Quarter 4, 2016). The employee must be employed by you for two consecutive full calendar quarters before you can claim a credit. Quarter 4, 2016 and Quarter 1, 2017 are consecutive full calendar quarters. Therefore, the employee must be employed by you through the end of Quarter 1, which is March 31, 2017, to earn you a credit.

- Monthly filers may claim the credit on their March 2017 return due April 25, 2017

- Quarterly filers may claim the credit on their Quarter 1, 2017 return April 30, 2017.

- Annual filers may claim the credit on their Annual 2017 return due January 31, 2018.

If you hired the qualified employee on October 15, 2016 (Quarter 4, 2016), you would not be able to claim a credit until the June 2017 return due July 25, 2017 or Quarter 2, 2017 return due July 31, 2017. That is because Quarter 4, 2016 does not count as a full calendar quarter since the employee was hired mid October. You count Quarter 1 and Quarter 2, 2017 as the first two full calendar quarters.

- Credits are claimed electronically through your tax filing account in the Department’s E-file system (My Account).

- Credits may be carried over until used, but must be claimed on returns filed no later than June 30, 2023.

- Credits will not be refunded.

What if I claim a credit and the statewide limit has been reached?

We will provide you written notice, if all or part of your credit claimed is disallowed. The notice will include the amount of tax to be paid within 30 days. If for some reason you do not pay the tax, penalties and interest will be assessed.

You may carry over the disallowed portion of your credit to the next fiscal year. However, you can only claim it if the cap for the next fiscal year is not exceeded. We will give credits carried over from a previous fiscal year priority when allowing businesses to claim credits.

What are the record keeping requirements?

You must keep records necessary for the department to determine if you are eligible for the credit, including records that show:

- The employee’s status as a veteran and…

- The employee was unemployed for at least 30 days when hired.

What happens if I have to dismiss the employee?

If you dismiss a qualified employee for whom you have claimed a credit, you may not claim a new credit for any employee one year from the date the qualified employee was dismissed.

This waiting period does not apply if the qualified employee was let go for misconduct (RCW 50.04.294) connected with his or her work, or let go due to a felony or gross misdemeanor conviction, and you thoroughly document the reason for the dismissal at the time.

Annual Tax Incentive Survey

You must electronically file an Annual Tax Incentive Survey every year you claim the credit. The survey is filed through your tax filing account in the department’s e-file system (called My Account).

The survey is due by May 31 of the year following the calendar year in which you claim the credit. For example, if you claim the credit on tax returns for periods in 2017, you must file a 2017 Annual Tax Incentive Survey by May 31, 2018 (RCW 82.32.585).

Definitions

“Full time” means a normal work week of at least thirty-five hours.

“Qualified employee” means an unemployed veteran who is employed in a permanent full-time position for at least two consecutive full calendar quarters. For seasonal employers, “qualified employee” also includes the equivalent of a full-time employee in work hours for two consecutive full calendar quarters.

“Unemployed” means that the veteran was unemployed as defined in RCW 50.04.310 for at least thirty days immediately preceding the date that the veteran was hired by the person claiming credit under this section for hiring the veteran.

“Veteran” means every person who has received an honorable discharge or received a general discharge under honorable conditions or is currently serving honorably, and who has served as a member in any branch of the armed forces of the United States, including the National Guard and armed forces reserves.

Questions?

- Credit questions: visit our Tax Incentives web page and select Employer Incentives.

- General tax questions: call our Telephone Information Center at 1-800-647-7706.

- Annual Tax Incentive Survey questions: call Taxpayer Account Administration at 360- 902-7167.